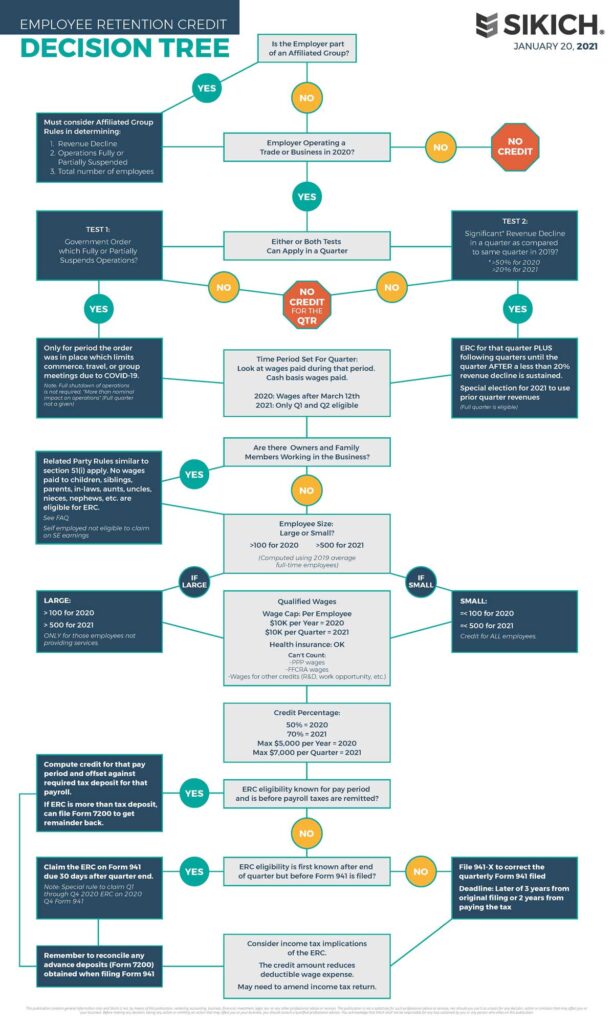

For 2020 ERC, the quarterly revenue decline needs to be more than 50%. To determine this, employers would compute their 2020 quarterly revenue and compare it to the same quarter for 2019.

For 2021 ERC, the quarterly revenue decline needs to be more than 20%. Employers would compare their 2021 quarterly revenue to the same quarter for 2019.

A special rule for 2021 ERC allows the business to look to the previous quarter to determine a revenue decline greater than 20%. For example, during the first quarter of 2021, the fourth quarter revenue of the previous year could be used (Quarter 4 of 2020 vs. Quarter 4 of 2019). This special rule would be used if Quarter 1 2021 revenues had not declined more than 20% from Quarter 1 2019 revenues.

A special rule for 2021 ERC allows the business to look to the previous quarter to determine a revenue decline greater than 20%. For example, during the first quarter of 2021, the fourth quarter revenue of the previous year could be used (Quarter 4 of 2020 vs. Quarter 4 of 2019). This special rule would be used if Quarter 1 2021 revenues had not declined more than 20% from Quarter 1 2019 revenues.

For a business that started in 2019, the quarter the business began should be the base of determining the quarterly decline, until the business reaches a year of operations. For example, a new business that started in the second quarter of 2019 would use that quarter as the base to determine revenue decline for either first quarter 2020 or second quarter 2020. If a business started in the middle of a quarter in 2019, an estimate of that period’s gross receipts can be used.

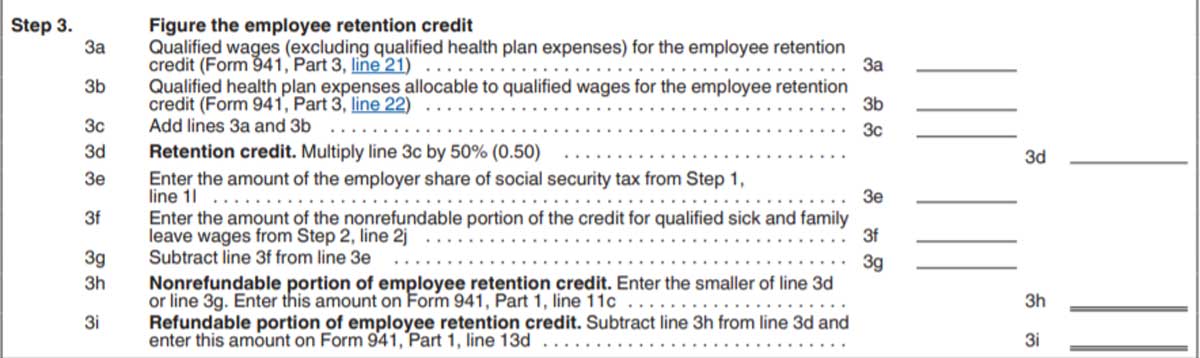

If you are a “small employer,” the ERC can be claimed on ALL employee wages (see employee wage limits in Question #6 below, and subject to family restrictions described next). See Question #5 for a further description of a “small employer.”

If you are a “small employer,” the ERC can be claimed on ALL employee wages (see employee wage limits in Question #6 below, and subject to family restrictions described next). See Question #5 for a further description of a “small employer.”

If you are not a small employer, the ERC can ONLY be claimed on wages paid to employees for not working. The definition of employees “not working” should be carefully reviewed with your professional advisors. Additional guidance is necessary to determine if employees are considered “not working” for purposes of their wages being eligible for the ERC.

Wages paid to certain related parties and owners are limited (under rules similar to Section 51(i)). Family members such as siblings, children, parents, grandparents, etc. are ineligible for this credit. IRS FAQ #59 lists the ineligible relationships:

- A child or a descendant of a child;

- A brother, sister, stepbrother or stepsister;

- The father or mother or an ancestor of either;

- A stepfather or stepmother;

- A niece or nephew;

- An aunt or uncle;

- A son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law or sister-in-law.

Ineligible wages also include wages paid to an employee with an ineligible relationship (described in the link above) to someone considered to indirectly own 50% or more of the business through a constructive ownership (under §267(c)). Spouses, brothers, sisters, ancestors and descendants are considered to have indirect ownership. Indirect ownership can also occur from ownership in other business entities such as corporations, partnerships and trusts.

The self-employment earnings of self-employed individuals are not considered qualified wages.